There are only two ways to make money in a SaaS business - bundling & unbundling. After software moved to the cloud, companies made billions peeling off specific features & products from mega-conglomerates who were still stuck in the pre-cloud era. Salesforce was the one of the first cloud-based SaaS solutions to capitalize on this.

Since then, a large number of software companies have been on the unbundling side of things. They follow the common startup advice to do one thing & do it really well. Take the example of Typeform, Slack, Loom, Trello, etc.

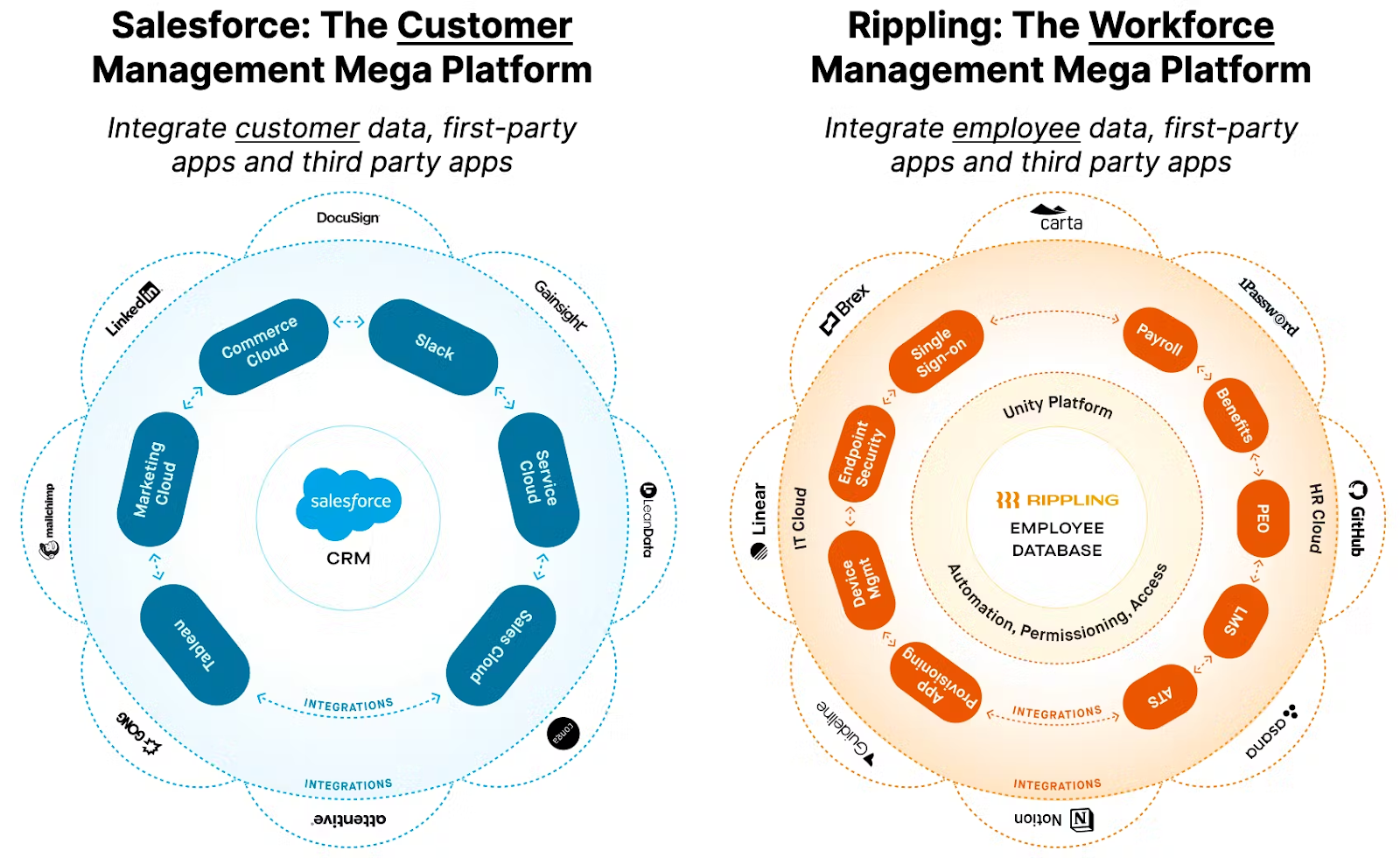

But software businesses of the future are moving towards bundling & becoming aggregators. The single-point solution of days past is now replaced by full-fledged platforms offered as a service.

Rippling is a company that falls under this category. It is the Salesforce of HR. Rippling is Salesforce, but starts from employee data rather than customer data.

Salesforce is a horizontal SaaS product operating in a specialized vertical, with customer data as the source of truth. Rippling is a horizontal platform operating in a specialized vertical with employee data as the source of truth.

The CEO of Rippling, Parker Conrad calls it a compound product.

Vertical SaaS solutions like Rippling aim to integrate the entire industry (HR in their case) and become the operating system for the whole market vertical. Rippling identified a problem common to the entire HR vertical - administrative tasks are a fundamental bottleneck to company growth.

Historically, employee data lived across multiple single-point solutions and workflows were scattered and time-consuming. Rippling's main value proposition is that it brings all administrative tasks under one roof.

It does this by using employee data as a focal point, which Rippling calls middleware. Any changes made in the employee data are automatically updated across all products across payroll, compliance, workflows, etc.

This approach has clearly been successful for Rippling. Rippling customers with 500-1K employees needed 24 people in HR and IT departments, compared to non-Rippling customers who needed 45 people in similar roles. Rippling has helped decrease HR and IT tasks by 96%, removed 15 hours of admin work a month and saved $50K in software costs for its customers.

This compound startup approach has clear advantages for Rippling.

- The multi-product approach helps build an ecosystem around Rippling the brand, with every product deeply integrated with each other.

- Every product is tied deeply to employee data since it is the single source of truth.

- They are more efficient & comprehensive since they can integrate product capabilities that are common to 30 different products by just building them once.

- It makes for a better user experience. Once Rippling customers get used to the UX, the entire ecosystem opens up for them. This also leads to high switching costs, creating a moat for Rippling.

- Rippling has a pricing advantage over point-SaaS competitors because they can optimize the cost of their software bundle rather than the price of any one single-product offering.

As of 2024, Rippling has generated $350 million in ARR and has recently raised $200 million in a Series F round at a $13.5 billion valuation.

Although Rippling has raised $1.4 billion over the last 7 years, it has never once used a pitch deck. Instead, Conrad writes investor memos, kinda similar to the ones Howard Marks uses at Oaktree Capital. Here is the 2024 memo that they used to raise their most recent Series F round.

Founding story

Parker started Rippling after a bad turn of events at his previous company Zenefits. Zenefits was a cloud-based SaaS that helped companies manage their human resource needs, like payroll and health insurance.

In two years, Conrad grew Zenefits to over $100 million in ARR across 10K customers. More than 90% of the company’s revenue came from the sale of health insurance. And then things went downhill. In November 2015, Zenefits was accused of allowing unlicensed brokers to sell health insurance. Conrad resigned as CEO in February 2016 after paying a hefty fine of $533k.

That same year, he launched Rippling along with Prasanna Sankar who was the CTO. They started building Rippling as a combination of (1) payroll, benefits, taxes (2) single sign-on, and (3) computer endpoint security.

The goal was to build software that could handle payroll, employee benefits & streamline the onboarding of new hires. They raised $7 million in their first seed round in 2017, with Initialized Capital being the lead investor.

The founders hired engineers and built the product for about 2 years in Parker's basement. They had a basic one-page marketing website mentioning Rippling.

In October 2018, they started cold emailing & reaching out to people & giving demos to them. They were targeting founders, CEOs, CTOs at the start, and as they continued to grow, scale, and expand, they started targeting HR decision-makers.

The sales system was designed in a pretty standard way - the client was passed on from the sales representative to the account manager to, eventually, the customer success manager.

Their CMO Matt Epstein was entrusted to fix the website and crystallize the messaging so users would "get" Rippling instantly.

This turned out to be very challenging since historically everything was unbundled. Payroll was different from IT, which was different from benefits, and so on. The messaging centered around how much time businesses could save by eliminating manual work.

Customers were also skeptical about how one platform could do so many things at once - was it a jack of all trades and master of none? And the interested customers didn't want to switch from their existing single-point solutions.

But they kept talking to customers. An early customer was an HR employee in the Midwest, who, halfway through the call in her thick Southern accent said "holy s**t! That is so cool. How are you doing that?" Customer calls like these gave them validation that they were onto something pretty big.

They got their first 100 customers just from sales-led outbound.

Six months after launch, the company raised 45 million in a Series A round, led by Kleiner Perkins. And yes, they didn't use boring pitch decks. Instead, Conrad wrote memos.

Growth & traction

Sales-led growth was still going strong for Rippling. By now, they had narrowed their focus to SMBs. They realized that 90% of people work for companies with fewer than 2,000 employees and in Canada & the UK the number was close to 99%, so Rippling chose to increase the ARPU (Average revenue per user) they can make from the larger SMB market.

Users would often come in looking for a single solution but sales reps on the call would show users why Rippling could solve the problem on a fundamental level & bring everything together in one place.

In 2018, Rippling was averaging 20% month-over-month ARR growth. That growth rate reached 25% in Q4 of 2018 & hit a growth rate of 29% in January 2019.

In 2019, Rippling’s net promoter score (NPS) was 70, as it was getting significant approval and recommendations from customers. That same year, they hired a VP of Brand who took on the role of rebranding Rippling. They spent close to 44 weeks on the rebranding, which was completed by 2020.

By August 2020, Rippling had grown to 250+ employees & had raised a Series B round with Founders Fund as the lead investor. Rippling was now serving 2500 customers reaching $13 million in ARR with a monthly ARPU of around $700.

In October 2021, Rippling had raised a $250 million Series C round at a $6.5 billion valuation. The same year, Rippling expanded its team to 800 employees and was serving a whole range of customers, from two-people companies to 1000+ companies. Its ARR at this stage was ~ $50 million.

It reached $100 million in ARR in May 2022 with a net dollar retention (NDR) of 200%. It means that for every $1 of revenue earned today, Rippling made nearly $2 next year as customers pay to use more of its products. For reference, the average public SaaS company has a NDR of 120%.

That same month, Rippling raised a $250 million Series D at a $11.3 billion valuation co-led by Bedrock & Kleiner Perkins with participation from YCombinator and Sequoia. By December of that year, they expanded to 1700 employees. By the end of 2022, it was at $175 million in ARR.

In March 2023, following the closure of Silicon Valley Bank, Rippling raised an emergency financing round to support its customers’ employees. It also raised $500 million in a Series E round led by Greenoaks.

By March 2024, Rippling had doubled its ARR to more than $350 million. However, the company was reported to be burning about $100 million per year at that time.

Rippling, the product

The main value proposition of Rippling the product is that it brings all administrative tasks under one roof. It does this by using employee data as a focal point, which Rippling calls middleware. Any changes made in the employee data are automatically updated across all products across payroll, compliance, workflows, etc.

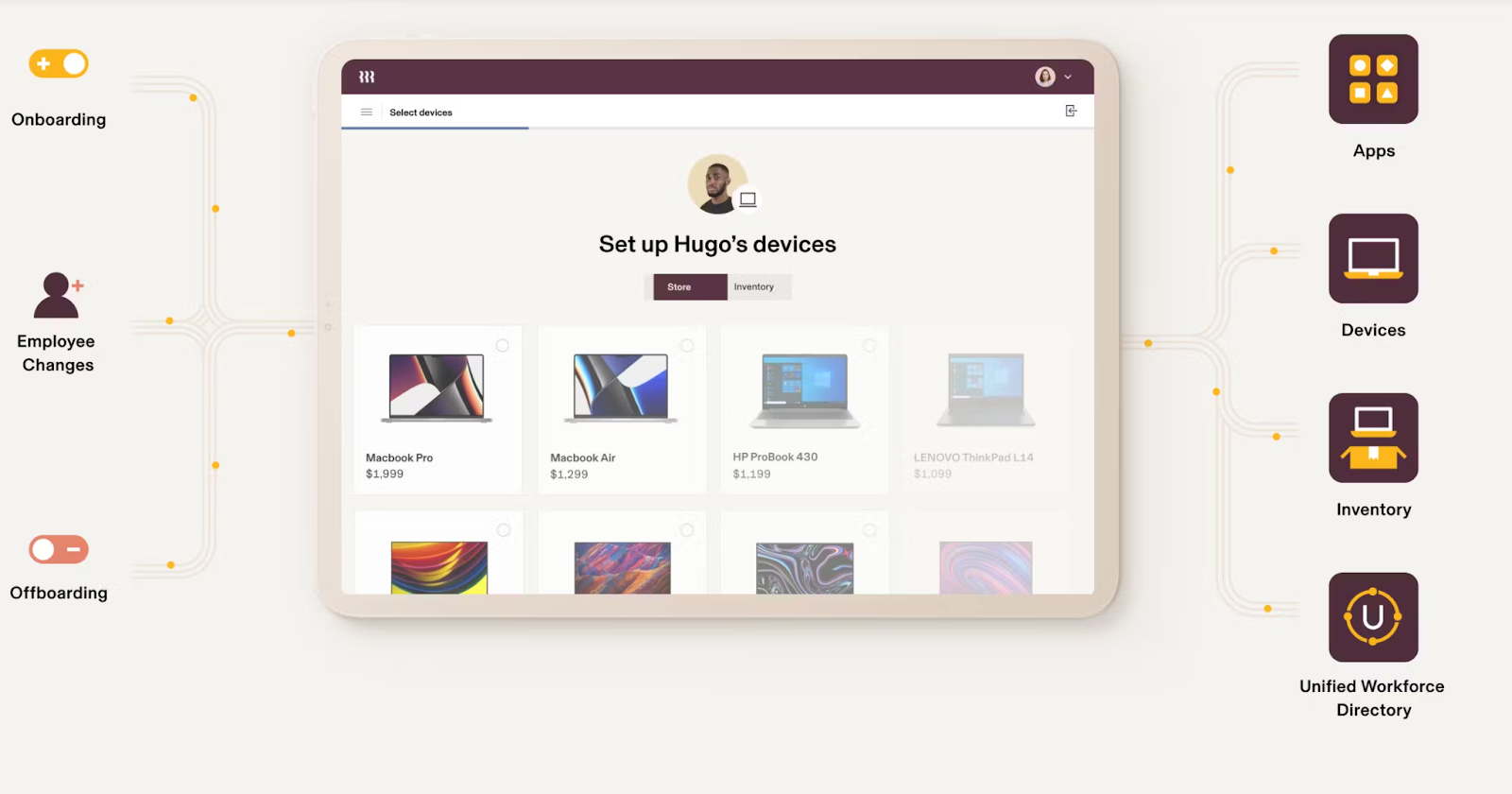

Since employee data is at the center of the product experience, Rippling’s product entry starts at the employee onboarding point. Via the employee onboarding process, Rippling collects all the necessary employee data such as social security numbers, location, salary, and manager information.

When a new employee is hired, Rippling automatically adds that person to payroll and to the company’s 401(k) plan. It ships a laptop preloaded with the right software to the person’s house. It gets the new hire the right tools for their job like Notion, Figma, and Github, depending on their role. Rippling also automatically puts them into the correct emails and Slack channels. All this happens in 90 seconds.

They have over 500+ integrations with third party software applications from Gong, Zendesk, Brex, and more.

Rippling has 3 main product pillars.

HR Cloud

Rippling offers multiple HR products including global payroll, benefits, recruiting, performance management, time and attendance, learning management, talent management, global employment, surveys, headcount planning, and compensation bands.

- Payroll: Payment, compliance, documents, tax filing, and more.

- Time Tracking - Approval, management, PTO, break tracking

- Talent Management - Recruiting, onboarding, learning, engagement

- Benefits - Connect existing plans, health insurance, 401(k), and more.

- Learning Management - Training, track progress, certification

- Recruiting - ATS, onboarding, exit offboarding

With Rippling, everything is synced across the entire product suite. So managers can simply review hours, PTO requests, and deductions from one place. Banking information is also synced via Rippling, so a manager can simply hit “Run” to process payments, file texts, and generate journal entries for bookkeeping.

IT Cloud

The IT product offerings allow administrators to manage applications, identities, devices, and inventory.

- App Management: App provisioning, SSO, password management, multi-factor authentication (MFA)

- Device Management: Device setup, device security, device offboarding, ordering, shipping & storage

Employers can not only set up and manage employee applications in one place but also deploy inventories to employees with a single click. Rippling takes care of all the shipping & logistics in the backend. Employees can manage all their applications from a single place.

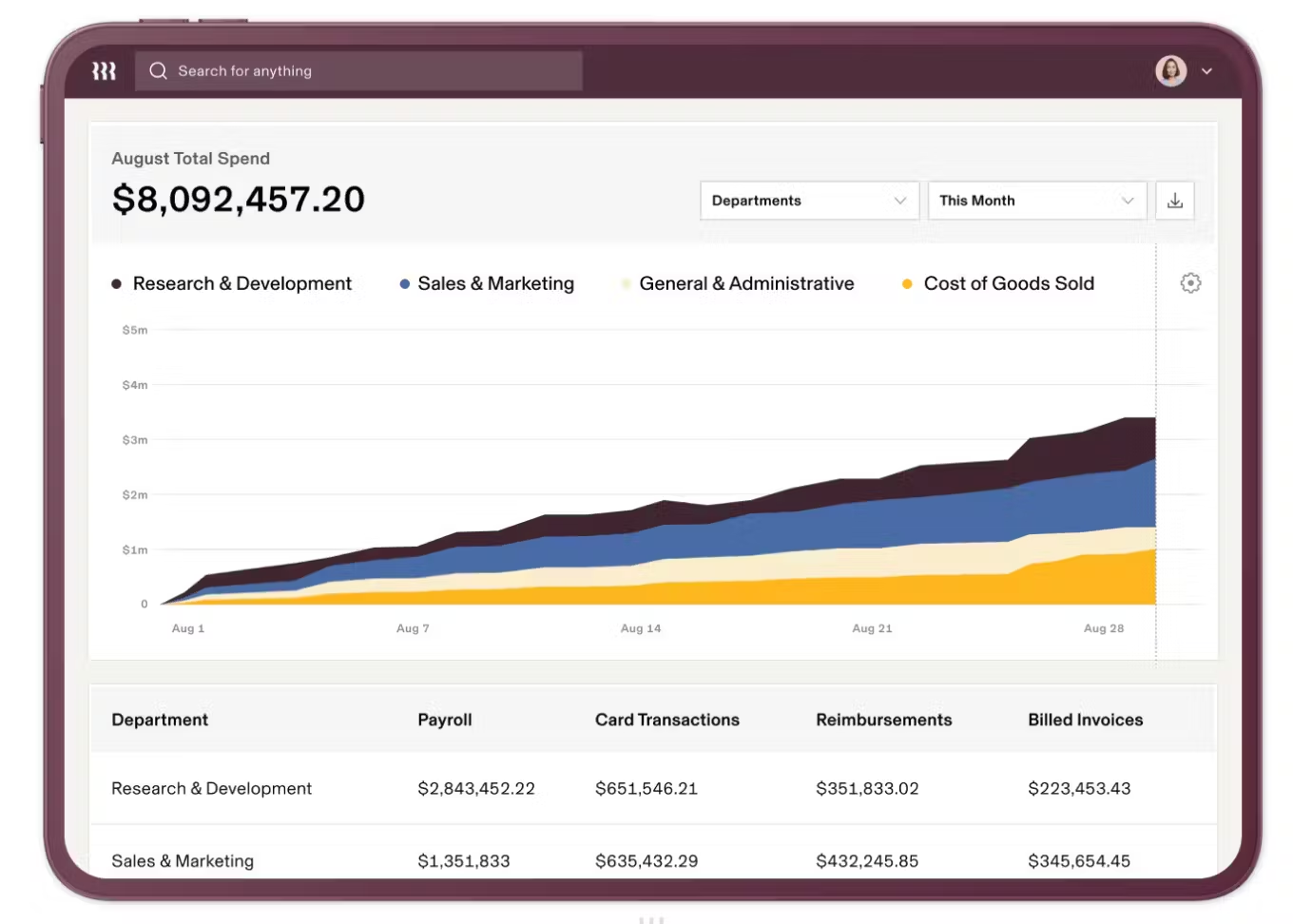

Finance Cloud

The Finance Cloud includes four key offerings: corporate cards, expense management, bill pay, and payroll management.

The corporate card allows companies to manage and issue physical & virtual credit cards, track card cycle automation, and control employee spend. Expense management is available in over 100 countries. With the expense management module, companies can pay out reimbursements, create custom policies and approvals. Companies can also automate payroll using the payroll management module. The bill pay product allows users to route, review, and approve bills.

Business model

Rippling is a platform as a service, and they charge a flat fee of $35 per month to access the platform. They have also set up a value-based pricing model where they charge a monthly fee for each user starting at $8.

One of the advantages of having a bundled application is that expansion revenue is more easily realized. In Rippling’s case, as their customers expand their business, they will pay more to access more of Rippling’s products. Rippling’s expansion revenue lies in expanding the number of seats their customers are paying for. Churn is also low due to high switching costs.

Rippling also has access to user data that they use to identify key events that lead to an upsell event. For example, companies typically look for expense management when they reach their 20th employee

Rippling also makes money from its 3rd party integrations with over 500+ SaaS products via a revenue-share split.

Conclusion

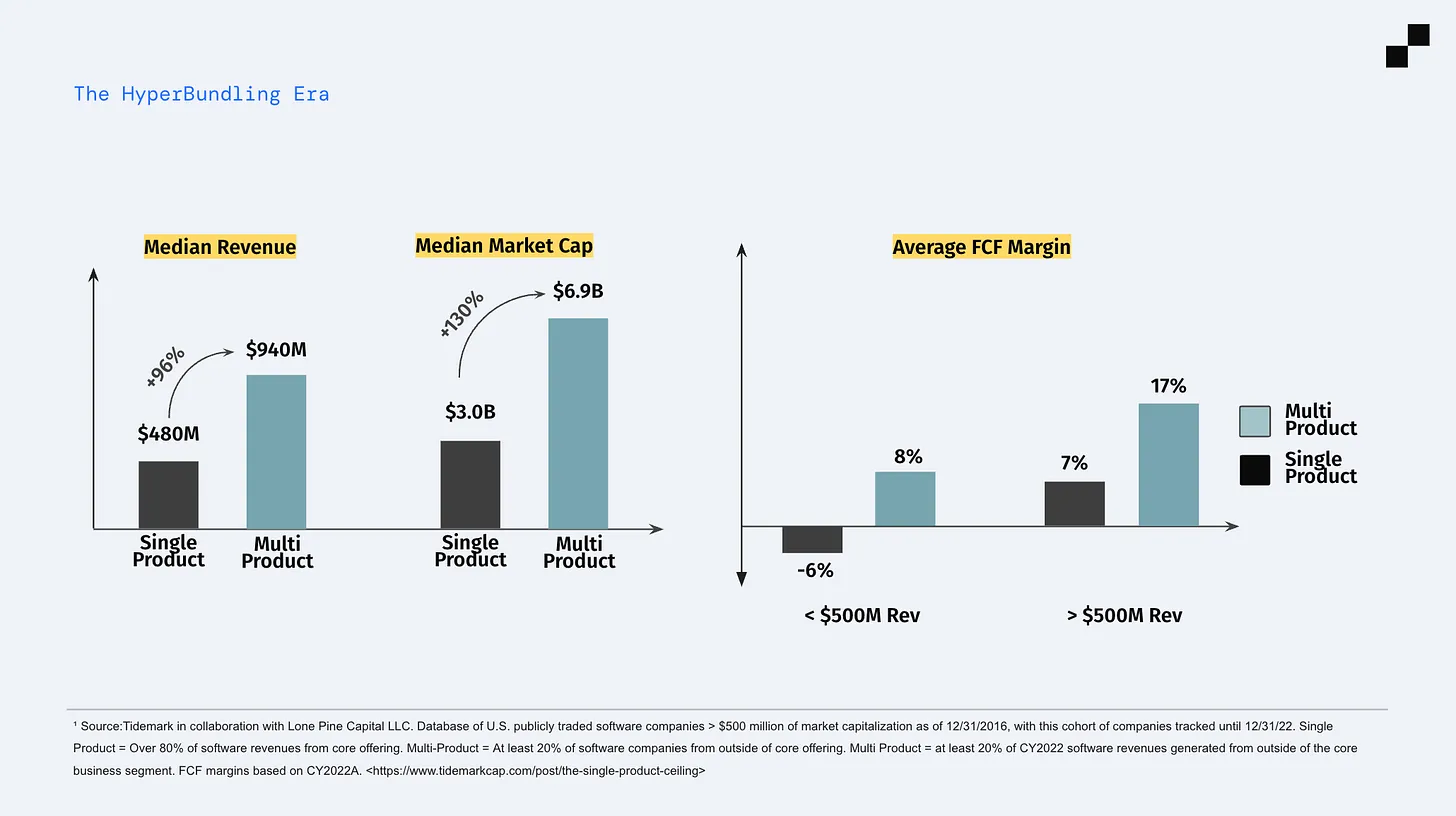

The rise of Rippling suggests that we could be entering the hyper-bundling era where bundling different products under a single platform is the new value addition for customers. Historically, point-based solutions have dominated the SaaS landscape. Investors have advised adopting a laser-focused approach to dominate a product category, often at the expense of the company's margins.

But there seems to be a law of diminishing returns at play here. Every product category is dominated by two or three players competing for similar customers. And each of those customers juggle multiple softwares in that niche. A product team would use Figma, Protopie, Galileo, Zepelin, Jira just to design a product.

This is causing both workflow management & subscription fatigue, leading to ICP saturation. This leads to diminishing returns aka a decrease in marginal sales and new bookings per dollar invested in customer acquisition. This isn't exactly good news for businesses either as CACs are going up with each passing year.

Data suggests that the median revenue for a multi-product SaaS is 96% more than a single-point SaaS. The market cap for multi-products is 130% more as well.

The average public SaaS company has a 28-month CAC payback period and a 10% operating margin as of March 2024. Rippling currently has an 8-month CAC payback.

Until 15 years ago, business software was purchased from a small number of companies like SAP, Oracle, and Microsoft. The shift to the cloud meant that competitors could unbundle specific features/products from these mega-vendors and turn them into standalone, point-SaaS companies.

Now that the cloud infrastructure has firmer roots, the advantages of deep systems integration and bundled contracting and pricing will dominate the market again. As such, a new wave of cloud-native mega-vendors is going to emerge. One of these is Rippling.

And it's not just Rippling that is riding the hyper-bundling era. Notion, too, is a (horizontal) compound product as it bundles features/products across project management, document creation & collaboration, calendar booking & more.

*Wink* *wink* We too, at CommandBar, have multiple products bundled together into two suites, the Assist and Nudge suites. You can learn more about our user assistance platform here.

It will be super interesting to see the evolution of the B2B software space in this coming decade especially with the rise of AI. Is the next trillion dollar company going to be a compound product? It might just be.